Altfi: how to scale part 2

This article was first published in Altfi: here.

PrimaDollar boss Tim Nicolle shares the secrets to scaling a start-up.

PrimaDollar is a global trade finance platform that is scaling quickly. A key question from all our stakeholders is: “How are you managing to scale?”. How to scale is the major challenge for all start-ups.

This is part 2 of our note on this topic. Part 1 introduces the issues and explains how dangerous the scale-up process can be for a start-up. Part 1 is available here.

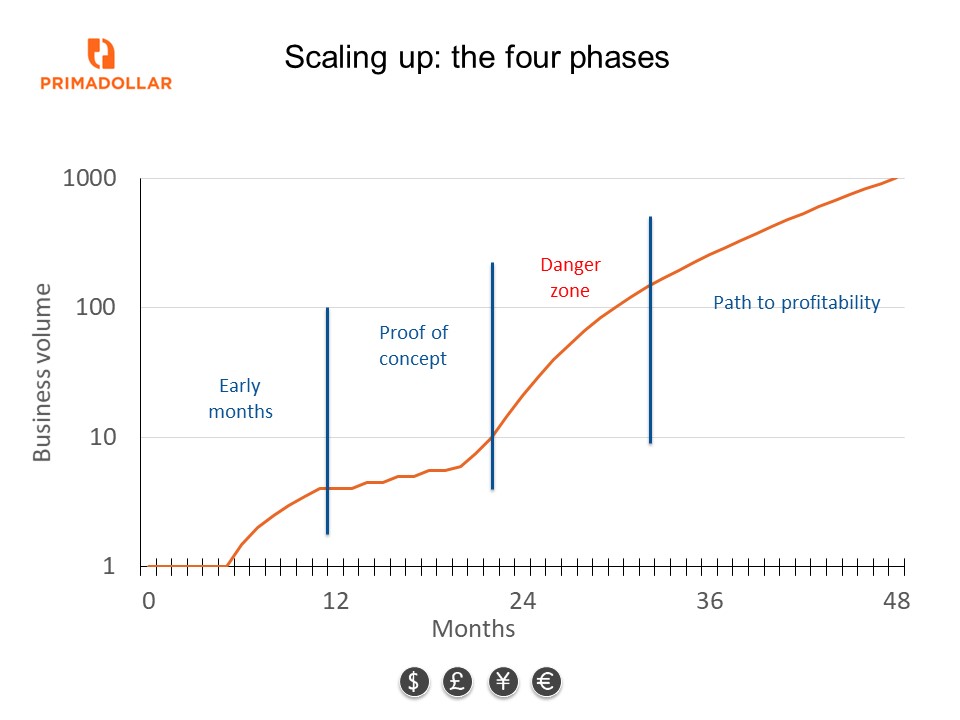

A reminder from part 1: The general formula for scale

There is a simple formula at work, “SECA”:

S = (E x C) – A

S is scale

E is enquiry volume

C is conversion rate

A is attrition

A reminder from part 1: The four phases of a start up

Phase 1: Early months – establishing the market opportunity, price points, delivery process etc.

Phase 2: Proof of concept – first trades are written, product is proven

Phase 3: Danger zone – scaling up by boosting enquiry or increasing the conversion rate

Phase 4: Path to profitability – the product is becoming adopted, trust is building, pricing is mainstream

What is the danger zone?

The danger zone applies to all start-ups. The danger zone is the initial scaling up period – a time when the business is not yet fully built, when costs are high because critical mass is yet to be achieved, and when there is pressure to grow by boosting conversion because enquiry is not where it should be.

As you will note from the formula, scale is achieved either by increasing enquiry or increasing conversion.

The danger zone: the example of alternative credit

A good way to illustrate the danger zone is to consider a credit business or a lending business. This could be a balance sheet business like PrimaDollar, a peer-to-peer platform or even a regulated business like a bank.

There are two big traps in the danger zone. Both traps relate to the conversion rate.

These two traps are:

- Push the conversion rate and write marginal business; typically this means more risk for less reward.

- Fail to manage adverse selection; filters on new business have to be more resilient to cope with the fact that early customers can be simply more risky than they seem.

The traps are real in the danger zone. At this time, the start-up or early-stage business is under pressure to grow, but it lacks the market reach, the deep pockets and the reputation. This means that generating more enquiry is difficult and relaxing the conversion rate becomes a major temptation.

Let’s look at these two traps in turn:

1. The marginal business trap:

If enquiry stays the same and a credit business scales, then the conversion rate must have gone up. The credit business has most likely taken on more risk, and just at a time when it is ill-equipped to deal with it.

There are a number of ways in which businesses might convert more enquiry, some of which are not obvious:

- flex the product design and / or go into new markets;

- compromise on the underwriting principles or take short cuts; this is easy to do if controls are yet not fully established

- fall into the trap of thinking that credit risk is someone else’s problem (for example, your funders, credit insurers, P2P investors)

- smoke your own stuff – assume that your algorithms and smart systems are capable of underwriting the business that the banks and others have turned down

All of these routes are nearly always going to be fatal. A credit business that scales up without generating more enquiry is simply taking more risk. If you would like to discuss examples or case studies of businesses that have gone wrong in the danger zone, please get in touch.

The only way to scale safely is to generate more enquiry.

2. The adverse selection trap

At this development stage, costs are usually higher than they should be. Selling with a positive gross margin is essential, otherwise the more you sell the more money you lose.

But selling with a high price can result in the enquiries being contaminated with adverse selection. Adverse selection means that your business is being sought out by poor quality clients. This happens if your proposition is targeted by, or is only attractive to, customers who have a higher risk (“adverse”).

This makes sense. Customers who are ready to pay an above-market price for a service are likely to be doing so for a reason. In a credit business, that reason is usually because the risk involved is high, perhaps higher than it appears on the surface. Moreover, this kind of customer is also the most likely to be getting in touch, and / or to be most enthusiastically chased by sales teams who are under pressure to deliver results.

At small scale, adverse selection may be invisible. But as a business starts to grow and cash starts to cycle back and forward to customers, buried risks can start to emerge.

Here’s the catch:

- Keep the price high and you get adverse selection.

- Price the product low to obtain a representative flow of enquiry, and you make less money; you might even lose money on trades and you can easily run out of equity before reaching any material size.

The right answer is to set the price low – and this may seem to be counter-intuitive. Whilst this approach has a risk, pricing low can move you quickly out of the danger zone or even avoid the danger zone altogether.

A lower price results in less adverse selection and can boost enquiry. At PrimaDollar, we call this strategy: “tomorrow’s price today”.

How do I scale quickly and safely?

Jump over or shorten the danger zone by following three simple rules:

Rule 1: Scale by increasing enquiry and not by converting more

Rule 2: Scale-up in line with enquiry; if you scale faster than enquiry, ask how

Rule 3: Monitor adverse selection, use the strategy “tomorrow’s price today”

These three rules will get you onto the path to profitability.

What should investors look for?

A lot of peer-to-peer platforms, alternative lenders, and new credit providers have been set up in recent years all over the world. Many are looking for capital, whether from retail investors or institutions, both debt and equity.

But many of these platforms are not scaling safely. Moreover, some platforms that have seemingly scaled up have not necessarily moved out of the danger zone, even if they are already sizable. Issues can be buried if lending is long.

Critically examine the business and apply the rules:

- Is this business scaling by increasing enquiry or by compromising on conversion rates?

- Is the business scaling faster than enquiry, and if so, how?

- Is this business correctly pricing its product, and also managing adverse selection risk?

How do these rules apply to PrimaDollar?

PrimaDollar’s market opportunity provides a way to implement these two rules, and with a trade finance solution that turns full cycle every 90 to 120 days, issues become visible very quickly.

- Our addressable market space is global trade, which we can address with a single, standardised product, without significant geographical restrictions. This means that we can increase enquiry simply by carefully expanding our footprint. We do not have to compromise on conversion – we can boost enquiry.

- We have arranged low cost capital markets financing in scale, which means that we can economically offer a low cost product. We can already offer “tomorrow’s price today”.

Of course, execution remains a challenge – it is a challenge in every business. But we are moving forward with every chance to get it right. We have moved out of the danger zone using these principles.

What about other types of business?

Other types of business should also remember the simple “SECA” formula:

S = (E x C) – A

Some of the dangers of adverse selection and increasing conversion rates may not apply to non-credit businesses. But the basic principle that a business cannot scale materially faster than its enquiry rate broadly remains.

Dealing with that issue and adopting a “tomorrow’s price today” strategy is brave, but probably the only real way to shorten the danger zone and get onto the path to profitability.